Mon 20th Apr 2026

The Quantum Ecosystem Isn’t Just Startups: Why “Core” and “Non-Core” Players Matter

Service: Patents

Sectors:

The organisations actually building the field.

Following our overview of the three main branches of quantum technology - computing, communication and sensing - this article looks at the organisations actually building the field. The OECD & EPO report “Mapping the Global Quantum Ecosystem” (December 2025) provides a useful lens: the distinction between “core” and “non-core” participants in the quantum landscape.

At first glance, quantum innovation appears to be driven by specialised startups. The OECD & EPO report suggests a more nuanced reality: while these firms are critical, most innovation, patenting and industrial capacity sits outside this “core” group.

A Two-Layer Quantum Ecosystem

Quantum technologies are often associated with specialised startups developing quantum computers or quantum sensors. In practice, the ecosystem is far broader. The OECD & EPO report identifies two main categories of stakeholders:

- Core quantum companies: organisations whose primary activity is the development of quantum or quantum-enabling technologies.

- Non-core organisations: companies, universities and public research organisations (PROs) that contribute to quantum innovation while pursuing other primary business activities.

Across the global landscape, the report identifies 4,622 organisations active in quantum, of which 830 are core firms. In other words, more than 80% of the ecosystem lies outside the core.

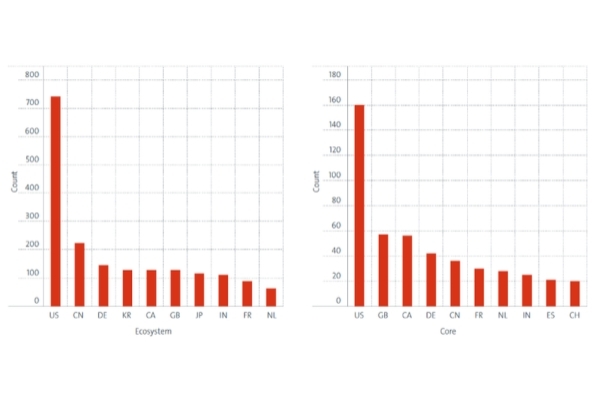

Figure 1: Number of firms in the quantum ecosystem entering the quantum field by country: 2015-2024.

This structural imbalance has important implications; while specialised quantum companies attract attention, the majority of patents, jobs and industrial activity in quantum technologies originates from organisations whose primary business lies elsewhere.

From a patent perspective, this distinction immediately becomes visible in the data.

What Defines a “Core” Quantum Company?

Core firms are typically young, research-intensive companies focused almost entirely on quantum technologies. Many are startups emerging from university laboratories or research collaborations.

Their activities fall into two broad groups:

- Developers of quantum technologies directly based on quantum physics (e.g. quantum processors, quantum communication systems, or sensing platforms).

- Enabling technology providers, supplying essential components such as photonics systems, cryogenics, or nanomaterials that make quantum devices possible.

These firms rely heavily on early-stage investment and public funding, reflecting the deep-tech nature of the sector. Indeed, around 71% of core quantum firms have received external funding, including grants, venture capital or IPO-related financing. Despite their relatively small number, these companies represent a concentrated hub of specialised innovation.

The Patent Footprint of Core Firms

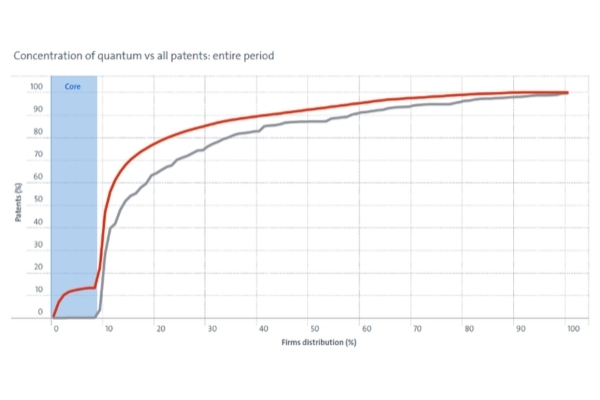

One of the most revealing statistics in the OECD & EPO report concerns patenting. Core quantum firms account for roughly 11% of quantum patents worldwide.

Figure 2: Concentration of quantum vs all patents: 2005-2024. Data refer to the distribution of IPFs (total and quantum) among quantum firms ranked by decreasing share of quantum patents, starting with the core quantum firms and then the remaining ecosystem firms.

At first glance this may appear modest, but the number is actually striking for two reasons:

- 11% is a notable contribution given their smaller scale and more limited resources compared to large multinationals.

- Core quantum firms are able to generate this considerable share despite having portfolios concentrated almost entirely on quantum technologies, as compared to large diversified companies whose patents span many fields.

In other words, core firms occupy a distinct position in the patent landscape: they generate domain-specific intellectual property rather than broad portfolios.

Computing Takes the Lead

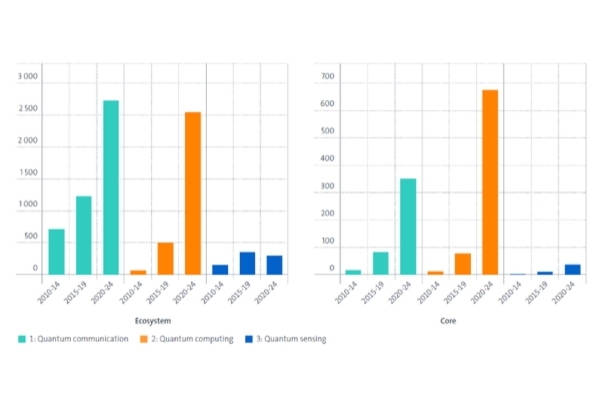

The report also highlights an important shift in the technological focus of the ecosystem. Historically, many early quantum companies emerged in quantum communication, particularly in areas such as quantum cryptography and quantum key distribution. Today, however, quantum computing has become the most prominent technology among core firms.

Patent trends confirm this shift. Patent growth has been strongest in quantum computing. Within the core ecosystem, computing-related patents are nearly double those in communication, while quantum sensing and metrology remain comparatively smaller fields.

Figure 3: Patents filed by quantum firms by technology: 2010-2024. Data refer to quantum IPFs filed by quantum firms in the whole ecosystem and by core quantum startups.

This suggests that specialised startups are increasingly concentrating on quantum computing platforms. This contrasts with large industrial players, who are continuing to pursue protection for communication technologies.

Geography of the Core Ecosystem

The geographical distribution of quantum companies also differs depending on whether one looks at the core or the broader ecosystem. Across the entire quantum landscape, the United States leads by a considerable margin, followed by countries such as China, Germany, Korea, Canada and the United Kingdom. Within the core segment, however, the picture changes slightly. The United States still dominates, but the United Kingdom and Canada play a more prominent role among core firms than they do in the broader ecosystem. This likely reflects strong university spin-out cultures and national research programmes supporting early-stage quantum startups.

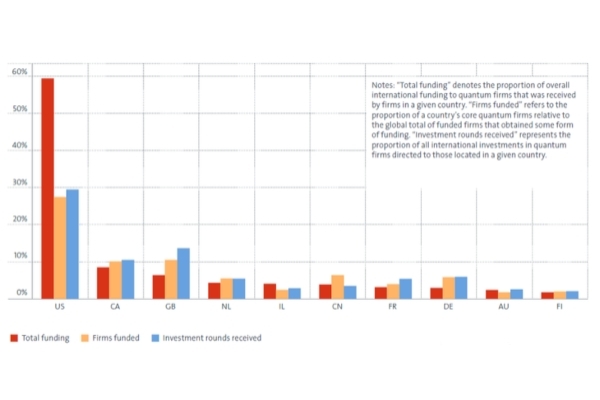

Funding patterns reinforce the US lead. Although the United States hosts around 30% of quantum startups, approximately 60% of global quantum funding has gone to US-based companies, primarily due to larger average investment rounds.

Figure 4: Country shares in global quantum funding, firms funded and investments rounds.

The Overlooked Majority: Non-Core Organisations

If the core firms represent the specialised research engine of the ecosystem, non-core organisations provide its industrial scale. These include large multinational companies, public research organisations, universities, as well as companies integrating quantum technologies into existing products or services. Together they account for over 80% of the quantum ecosystem and generate most quantum-related patents and job postings.

Large technology companies such as IBM, Microsoft, Intel, LG Electronics and Toshiba are among the most prolific patent filers in quantum technologies. Their role is particularly significant for commercialisation. Unlike startups, these organisations already possess manufacturing capabilities, global supply chains and established customer bases. When quantum technologies reach industrial maturity, they are well positioned to integrate them into existing products and services.

Patent Concentration in Quantum Technologies

Another striking observation from the report concerns the concentration of patent ownership. Approximately 20% of patent holders account for around three-quarters of all quantum patents, a higher level of concentration than in patenting overall.

This concentration reflects the technical barriers to entry in quantum technologies, which require specialised expertise, advanced laboratory infrastructure and substantial capital. However, it also raises broader questions about how widely accessible quantum innovation will be as the technology matures. For patent practitioners, this concentration suggests that key foundational patents may remain in the hands of a relatively small number of organisations, shaping licensing strategies and competitive positioning across the sector.

Where Core and Non-Core Players Meet

Although the ecosystem is divided conceptually into core and non-core organisations according to the OECD-EPO report, the two groups are deeply interconnected.

- Core firms often translate fundamental research into early-stage technologies, frequently emerging from university environments.

- Large companies and research institutions provide scale, infrastructure and application pathways.

The balance between these groups varies across countries. Some ecosystems rely heavily on scaling startups, while others benefit from the early involvement of established industrial players. In practice, the growth of quantum technologies depends on both layers of the ecosystem evolving together.

What This Means for the Future of Quantum Innovation

The OECD–EPO analysis makes one point clear: the quantum sector cannot be understood solely through the lens of startups or specialised quantum companies. Instead, it is characterised by a two-tier ecosystem: a small but highly specialised core of quantum technology developers, and a much larger set of organisations integrating, applying or supporting those technologies.

From an innovation and patent perspective, this structure has several implications:

- Specialised startups are driving many of the foundational breakthroughs, particularly in quantum computing.

- Large diversified companies remain the dominant patent holders, shaping the intellectual property landscape.

- Collaboration between research institutions, startups and industrial players will remain central to the commercialisation of quantum technologies.

As quantum technologies continue to mature, the interaction between these two layers of the ecosystem will likely determine how quickly, and how broadly, the benefits of quantum innovation are realised.

Next week we will examine how investment trends are shaping the quantum industry and what they reveal about the commercial trajectory of the technology.

To protect your quantum innovations, please contact Tom Mahon.

This briefing is for general information purposes only and should not be used as a substitute for legal advice relating to your particular circumstances. We can discuss specific issues and facts on an individual basis. Please note that the law may have changed since the day this was first published in April 2026.