Wed 29th Apr 2026

Investment Trends behind Quantum Innovation

Service: Patents

Sectors:

Damon Ho and Dr Shameena Bonomally explore what is fuelling startups in the quantum ecosystem

Our last article looked at the organisations shaping the quantum ecosystem, focusing on the distinction between core players – startups dedicated entirely to quantum technologies – and the non-core players whose main business lies elsewhere. This week, the spotlight shifts. We move from who is building quantum to what is fuelling them. When looking at questions about capital, commitment, and commercialisation, we once again draw from the joint report from theOrganisation for Economic Co-operation and Development (OECD) and the European Patent Office (EPO), “Mapping the Global Quantum Ecosystem” (December 2025). This third piece examines where investment is flowing and how governments are reshaping the domain.

Government Funding is rising

Governments often step in early in strategic technologies, and quantum is no exception. Public R&D funding for quantum innovation has climbed steadily from approximately 0.4% of total government R&D budgets in 2015 to 1.1% by 2023, awarding funds to a total of 12,209 quantum-oriented R&D projects. Many governments have recognised the potential of quantum technologies and developed relevant initiatives such as the National Quantum Initiative Act in the US and the Quantum Technologies Flagship in the European Union.

Beyond R&D grants, governments are using procurement to create early demand. For instance, Pasqal, a French quantum computing company, has installed quantum systems in high-performance computing centres across France, Germany, and Saudi Arabia through public procurement programmes such as EuroHPC. This model allows governments to accelerate technical maturity and market adoption whilst providing operational feedback from real users. For core quantum firms, government as a first customer may prove as important as government as a funder.

The report is clear, however: public money alone will not bring quantum to market. The transition from basic research to industrialisation and early commercialisation requires deep private-sector involvement.

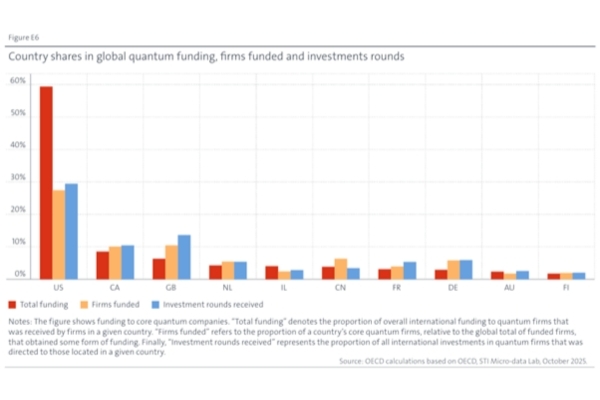

One Country dominates the Investment Landscape

When looking at global quantum funding, countries typically have a similar proportion of total funding, firms funded and investment rounds. It comes as no surprise, however, that the US has set itself apart in this front. As home to about 30% of all quantum international patent families (IPFs) and startups, 60% of all quantum funding ever recorded has gone to US-based companies (see Fig. E6). That discrepancy reveals a simple truth: American quantum firms are not just more numerous but also attract consistently larger deals.

The Funding Gap between the US and Europe

The report shows that European countries (France, Germany, the Netherlands and the UK) have a solid base of quantum startups. Europe, which has significantly increased their share in total quantum investment over time from a smaller base, attracts substantially less investment than their US counterparts. Alongside total volume, the gap also covers the nature of the investment.

US-based investors back companies across the full funding lifecycle, whereas in most other countries see a higher share of funding coming from early investment stages such as grant, seed, and early-stage venture capital. The share of early-stage investment in 2021-2024 was observed as above 50% in all countries except the US and Australia. This imbalance suggests that the quantum domains outside of the US are struggling to provide the later-stage capital necessary for companies to scale into global competitors.

Specialisation in Quantum Technology

The revealed technological advantage (RTA) compares a country’s patent share in quantum to its global patent share, indicating whether a nation is genuinely specialised in quantum relative to its overall patent output. An RTA above one signals an above average specialisation. Canada and the United Kingdom both boast strong RTAs and dense clusters of core firms. Germany, Japan and Korea offer broad industrial bases and rich patent portfolios, with Korea standing out particularly in quantum communication. Meanwhile, the internationalisation rate of quantum patents – the percentage of IPFs compared to all patent families – stands at 31.2%, far above the 12% average for all technologies. That figure speaks to the intense global competition and high strategic stakes currently taking hold of the domain.

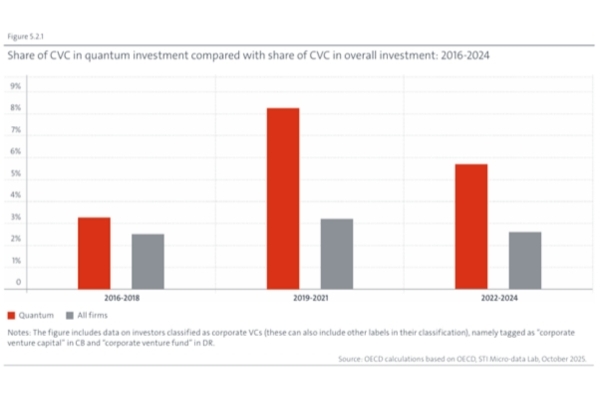

Corporate Venture Capital (CVC) and Merger and Acquisition (M&A)

Established companies are already taking direct stakes in quantum companies. Corporate venture capital (CVC) accounted for as much as 8% of quantum investment in the 2019–2021 period, more than double the CVC share across all industries (see Fig. 5.2.1).

These are not passive investments. The high share of CVC investment within quantum highlights the potentially transformative technology for many industries. The report notes that CVC investment flows almost entirely into quantum computing and communication, with virtually no CVC investment directed at sensing – revealing where the industry will likely see the earliest and largest returns.

Approximately 5% of core quantum companies have undergone an acquisition. Most M&A activity targets US-based companies, with around 9% of all US core firms being acquired. US companies are also the most active acquirers, including cross-border purchases of Canadian and UK-based firms. This suggests that the US is not only the largest source of startup creation but also the primary destination for consolidation, potentially pulling talent and technology from other ecosystems.

The Holistic Consideration

This week’s look at finance and policy shows a field divided by geography. The US leads in total firepower, but Canada, the UK, Germany, Japan and Korea each hold notable levels of quantum specialisation. Governments have kicked the ball rolling with public funding, initiatives and procurement to encourage development. And an ever-present emphasis on where and how private capital continues to fuel the industry will likely determine the extent to which quantum technology is reliably scaled and transitioned into a commercial reality in the coming decade.

We shift focus once again next week, inspecting the essential inputs and potential bottlenecks that support global supply chains behind quantum technologies.

To protect your quantum innovations, please contact Tom Mahon.

This briefing is for general information purposes only and should not be used as a substitute for legal advice relating to your particular circumstances. We can discuss specific issues and facts on an individual basis. Please note that the law may have changed since the day this was first published in April 2026.